Starhill REIT

With my recent interest in REIT, I decided to take a deeper look into another seem "promising" REIT, Starhill which is among the few available in the market now.

Starhill REIT is currently owned 51% by YTL corp while only 49% is from public. Assets of Starhill REIT are Lot 10, Starhill Gallery and JW Marriott Hotel, which are all strategically located within the golden triangle of Klang Valley. Both Lot 10 and Starhill Gallery are currently enjoying near full occupancy rate, with majority of leases expiring by 2008.

Starthill REIT has indicated that they will distribute near 100% of income as dividen for the period to 1H FY2007, and thereafter 90% for each financial year. For the latest income distribution announced during end of last month (1H FY2006), which is 3.4524 sen per unit, it representing approximately 100% as what they have claimed. If Starhill can maintain the same income for the full FY2006, this will translate to ~7.5% yield, which is attractive.

However, if one delved into more details of Starhill, one will observe its future potential is limited. Firstly, the management of Starhill REIT (which is Pintar project Sdn Bhd, 70% subsidiary of YTL Land) has no plan to aggressively acquire new property (besides those owned by YTL) into its portfolio to improve its yield.

Secondly, the rental hikes of all current 3 properties of Starhill are very limited. JW Marriot Hotel only provides ~1% rental hike annually; Autodome, which is a subsidiary of YTL contributes ~67% rental income for Starhill Gallery, thus there is a conflict of interest for any rental hike; and Lot 10 is unlikely to fetch any significant increase in rental due to stiff competition nearby, e.g. Berjaya Time Square etc.

Thirdly, the distribution rate after 1H FY2007 will be reduced to 90%, effectively lower its overall yield.

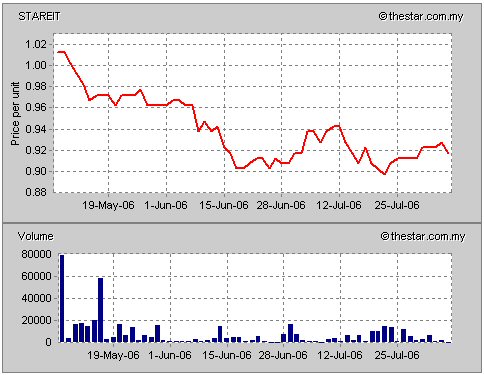

With all the above factors and unfavorable interest rate outlook for REIT in the past 6-9 months, its share price has dropped from its peak of RM1.07 to now RM0.915, which is below its IPO price of 0.980. NAV per unit as of 4-Aug-06 is quoted at RM0.983, about 6.9% lower than its current share price.

I personally think that the annual yield for Starhill will remain at ~7% until 1H 2007 base on its current share price of RM0.915. After that, I believe that its yield will drop to 6% or below due to reduced distribution rate and bleak outlook for shopping mall related properties when economy takes a downturn. It will be worse when the bulk of Lot 10 and Starhill Gallery leases expired by 2008, if recession happened at the same time.

As such, taking into account also the risk of depreciating share price, I personally will only consider to buy Starhill REIT for short term (1 year or less) if its share price hits 86 sen or less. This will fetch a yield of ~8%, and at the same time, minimizing the downside risk for capital preservation.

This blog is best viewed with Firefox browser. Download link at side bar.

Labels: Other Investment, Stock Market

posted by velo at 1:36 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home